On August 15th FHA released its Back to Work program. This new program allows borrowers who have experienced an economic event that “resulted in severe reduction in income due to a job loss or other circumstances” to obtain an FHA-insured mortgage just one year following the loss of a home via a pre-foreclosure sale, deed-in-lieu, or foreclosure with a short sale, bankruptcy, or restructured debt. See Mortgagee Letter 2013-26 for complete details.

FHA has always had a list of extenuating circumstances that make it possible for borrowers to obtain an FHA insured mortgage just one year after foreclosure (or deed-in-lieu of foreclosure). See HUD Handbook 4155.1 4.C.2.f – Previous Mortgage Foreclosure. Some examples of these extenuating circumstances, which must be beyond the control of the borrower, are a serious illness such as a heart attack or the death of a wage earner. Now, FHA has added “economic event” to this list.

Highlights of the Back to Work program:

- It applies to purchases only; does not apply to refinances.

- The homeowner must complete a HUD-approved homeownership counseling program at least 30 days prior to a new loan application.

- An acceptable Housing Counseling Certificate must be submitted with a new loan application.

- Certificates are good for six months. (Note: Contact me for a list of agencies, locations, and times for this counseling program.)

- The property lost due to foreclosure, etc. must have been a primary residence at the time of the economic event.

- A borrower MUST be able to document the economic event. This is very important.

- This program became available August 15, 2013 and will end on September 30, 2016.

- This program is only available for FHA case numbers pulled on or after August 15th, 2013.

Although the guidelines for qualification are strict, this can be a great opportunity for those who qualify. FHA is responding and adapting to the market as it is today. As FHA states, “FHA recognizes the hardships faced by these borrowers, and realizes that their credit histories may not fully reflect their true ability or propensity to repay a mortgage.”

Per the HUD Handbook 4155.1 4.C.1.a, FHA recognizes that, although past credit performance is a useful guide to determining a borrower’s attitude toward credit obligations, it may not reflect the whole story. FHA underwriters are encouraged to consider a borrower’s overall pattern of credit behavior, not just isolated occurrences of unsatisfactory or slow payments. It’s about assessing risk. Will the money be repaid?

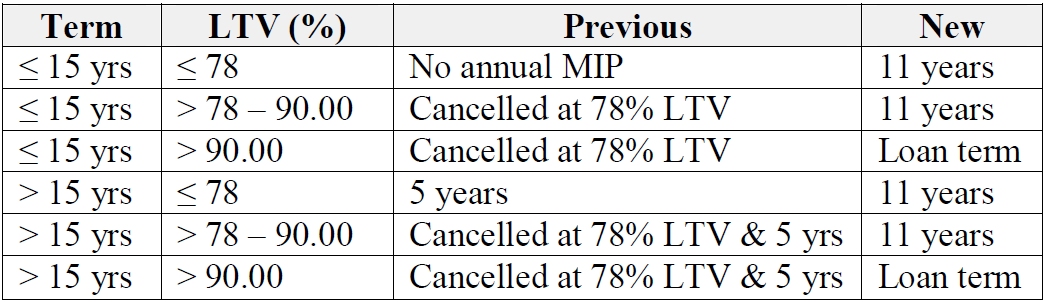

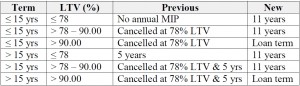

On June 3, 2013, FHA rescinded its automatic cancellation of the annual MIP (also known as never-ending monthly mortgage insurance) for most of its programs. See FHA Mortgagee Letter 2013-04. This new mortgagee letter introduced increased mortgage insurance rates, effective for case numbers pulled on or after April 1, 2013.

Back in the old days, if you took out an FHA fifteen year fixed loan with an LTV at or below 78%, you did not pay monthly mortgage insurance. Now, for those loan types with case numbers pulled on or after June third, there will be monthly mortgage insurance of 45 bps (basis points). See the chart below for a comparison of both old and new guidelines for mortgage insurance premiums and durations.

Previous and New Duration of

Annual MIP by Amortization Term and LTV Ratio

Exceptions to MIP Duration Changes:

Exceptions to MIP Duration Changes:

Title I, and Home Equity Conversion Mortgages (Reverse Mortgages)

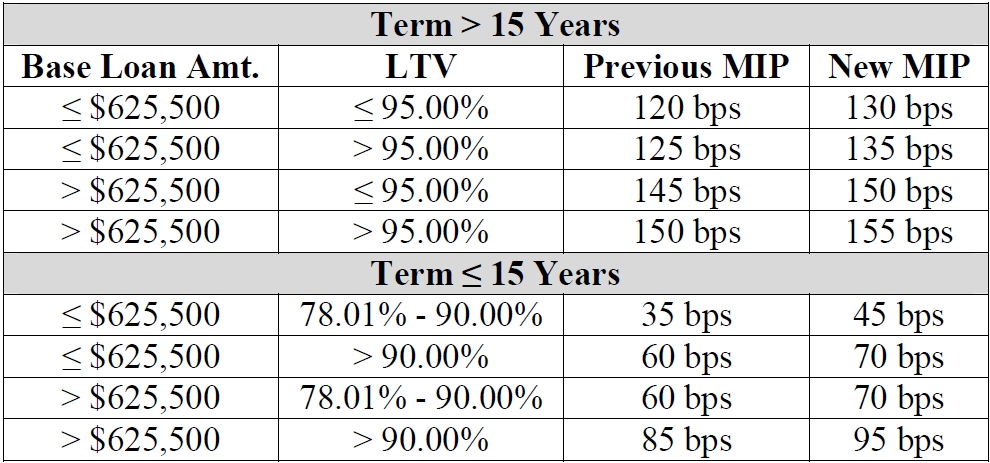

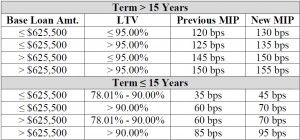

Previous and New Annual MIP Rates

by Amortization Term, Base Loan Amount, and LTV Ratio

Effective for Case Numbers Pulled on or after April 1, 2013

Previous and New Annual MIP Rates

For Loans with LTV Less Than or Equal to 78% with Terms up to 15 Years

Effective for Case Numbers Pulled on or after June 3, 2013

Exceptions to MIP Increases:

Streamline Refi’s of FHA Loans Endorsed on or before 5/31/09,

Title I, and Home Equity Conversion Mortgages (Reverse),

Hawaiian Homelands, and Indian Reservations

You might be asking why FHA did this? Why did they create never ending monthly mortgage insurance?

Well, because they are in the red, they are hurting badly. There have been rumblings about the financial security of the FHA Mutual Mortgage Insurance Fund for quite some time. FHA is still reeling from its losses during the housing bubble. At one point in 2012 there were even talks of a government bailout for this almost 80 year old entity. Low performing loans and seniors who are technically in default due to unpaid taxes and insurance are just a couple of the issues that have led to FHA’s problems.

However, FHA has made several moves to shore up its fund. It raised up-front mortgage insurance and annual premiums a few times, it sold non-performing notes, it ended seller-funded down payments, it introduced risk-based pricing (in the old days the interest rate on an FHA insured mortgage was unaffected by a low fico score), it modified its guidelines to make qualifying harder, and it restructured its reverse mortgage programs to limit cash out and encourage seniors to select healthier, better-performing reverse mortgage products. FHA has seen healthier business on its books since 2009, but the improvements didn’t come in time to prevent more extreme forms of curtailment.

Therefore, in its effort to adapt rather than go extinct, FHA giveth and FHA taketh away.